Land is often an incredibly valuable asset. However, for many property owners, their land and its future represent more than simply a dollar value on a balance sheet.

For some, their property is a culmination of family memories and lifetime achievements. Others may feel a strong desire to be good stewards of the health of the land they own and the natural resources on it, such as forests or bodies of water. Regardless of the reason, protecting property for future generations is often a primary consideration for landowners who wish to preserve their legacy.

Conservation easements are a powerful planning tool for safeguarding land indefinitely while simultaneously providing tax deductions in the short term. Unfortunately, because this tool is so powerful, some bad actors seek to abuse the system. Land developers committing easement abuses recently found themselves on the Internal Revenue Service’s annual Dirty Dozen list. The IRS is now enforcing new restrictions designed to curtail further exploitation.

It is important for landowners to understand potential abuses and pitfalls of conservation easements. This will help them ensure their compliance with IRS rules while realizing the full tax benefits for protecting their land.

Conservation Easement Basics

Intended Use

Conservation easements are not new tools in tax and estate planning. In fact, the earliest laws allowing for them were enacted in various states as early as the 1960s. However, it was not until the 1980s, when Congress created permanent tax subsidies for the donation of conservation easements to land trusts, that land trusts and conservation easements became widely popular. According to Land Trust Alliance estimates, from 1998 to 2003 the number of local and regional land trusts in the United States increased from approximately 1,200 to nearly 1,600, and conservation easements were estimated to have increased from 7,400 to about 18,000. (Note that the linked article requires a free JSTOR account to view.) Twenty years on, the National Conservation Easement Database has tracked more than 221,000 easements. This number may exclude certain private arrangements the organization cannot observe, but even so, it makes clear that conservation easements have continued to grow.

At its core, a conservation easement is a voluntary legal agreement between a landowner and a qualified nonprofit organization or government agency. The agreement establishes specific restrictions on the future use of some or all of the land, in perpetuity. The goal of a conservation easement is to keep natural lands from being developed to protect open spaces, to offer habitats for wildlife and natural flora, and to preserve sites of historical significance. In contrast to an outright gift, the current owner of the land retains the ownership and right to use their land, as well as the right to sell the land or pass it down to heirs.

For the recipient organization’s part, the main benefit is conserving land that a private owner might otherwise be reluctant to sell or donate. To secure this goal, the organization takes on the responsibility of making sure the stated conservation goals are upheld, by both monitoring the land and enforcing any restrictions on it. The organization will also coordinate with future owners to ensure that they understand the easement’s restrictions and abide by them.

Perpetuity is a key function of the easement. The restrictions placed on the land from the easement remain in effect even if the land is sold or inherited. This means that, while owners retain use of the land in its current state, they are giving up other potential uses for the land for their heirs or future buyers as well as themselves.

Since a conservation easement involves giving something up, even if it is not an outright gift, property owners may take a charitable deduction on their federal income tax return for donating conservation easements to qualified organizations. The value of the easement for tax purposes is determined by the difference between what the property would be worth if used for its “highest and best” use before the easement and the value of the property after the easement.

The deduction successfully incentivized the conservation of environmentally important land, as the growth in easements’ popularity demonstrates. The tax benefit is clearly attractive enough to encourage landowners to use easements as a tax planning tool. If your goals align with a conservation easement’s outcome, it is a strategy worth pursuing — but it is important to understand the specific rules the Internal Revenue Code lays out to maintain compliance with the law.

Criteria And Restrictions

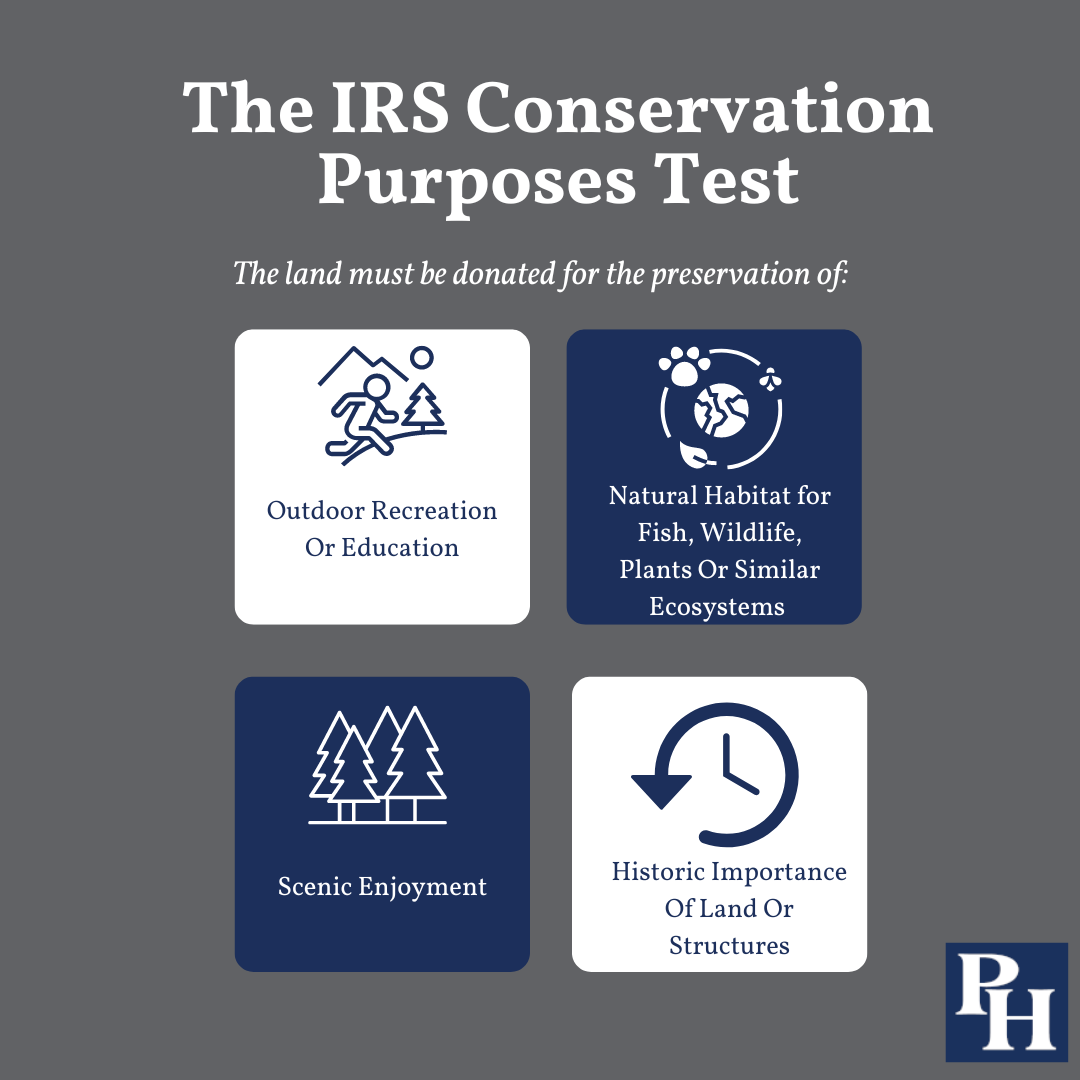

Ultimately, landowners must donate the easement with the intent to preserve or protect land for conservation. Donating the land without such a purpose undermines the intent of the conservation easement, and the gift would be immediately disqualified from the tax deduction benefit. The IRS measures intent through any one of the following “conservation purposes tests.” The land must be donated for the preservation of:

- Outdoor recreation or the education of the general public

- A natural habitat for fish, wildlife, plants or similar ecosystems

- Farmland, forest land or open space, where such preservation is for the scenic enjoyment of the general public

- Historic importance of land or structures

Once the conservation purpose of the easement has been established, you must ensure that the easement agreement is both voluntary between all parties and a qualified real property interest. This means the easement must cover all outstanding interests in the property. For example, if multiple people own the property, all of the owners must join in granting the easement.

In addition, as we mentioned previously, the conservation easement must be donated to a qualified organization to obtain the tax benefit. A qualified organization is recognized by the IRS as a publicly supported 501(c)(3) charitable organization or other donee permitted by the tax code. It is important to note that under Internal Revenue Code Section 170(h)(3), a private foundation is specifically ineligible to receive a conservation easement. Nancy A. McLaughlin, of the University of Utah S.J. Quinney College of Law, observed that legislators felt that “conservation easements donated to private foundations were less likely to be enforced and, presumably, less likely to provide benefits to the general public.” More generally, qualified organizations must demonstrate a commitment to protect the conservation purposes of the donation and must have the resources necessary to enforce the restrictions placed on the land. Some examples of qualified organizations are local land trusts, state fish and wildlife departments, the National Park Service, and Native American tribal governments.

Finally, to qualify for the tax deduction, the agreement must stand in perpetuity. This means the land will be committed to a conservation purpose forever, regardless of the land’s future ownership.

Although conservation easements are not the only option to protect your land for future generations, it is one of the most tax-advantaged options that will allow you to retain ownership. Some alternate methods, such as fee ownership and outright donation of the land, can also offer protection, but may require you to sacrifice ownership or forgo tax advantages.

Tax Planning Benefits

If an easement is qualified according to the Section 170(h) (the rules we have discussed in the previous section), the donated easement’s value becomes an allowable charitable deduction against your taxable income. As a reminder, the easement’s value represents the spread between the property at its “highest and best” use before the easement and the value of the property after the easement.

Before you can claim the deduction, the land must first be appraised by a certified appraiser according to IRS requirements. The IRS requires qualified appraisals for all contribution deductions for conservation easements valued at more than $5,000, although in most cases they need not be attached to your return. You should keep a copy for your records. For charitable deductions claimed on easements worth more than $500,000, or for deductions based on easements on historically significant buildings, you must attach a copy of the property’s qualified appraisal to your income tax return for the year when you claim the deduction.

Once the land has been properly appraised, the easement donation qualifies as a noncash charitable contribution for tax purposes. Taxpayers report conservation easements, along with other noncash contributions, on Form 8283, Noncash Charitable Contributions. Congress passed legislation in 2015 that permanently limited the allowable deduction of the value of conservation easements to 50% of a taxpayer’s adjusted gross income, or 100% of AGI for certain ranchers or farmers, in a single tax year. Taxpayers may carry forward any unused portion of the easement valuation for up to 15 years, compared to the standard five-year carryforward period for other charitable donations.

Note that, in addition to the income tax benefits, a conservation easement may offer the added benefit of lowering your taxes on the property in question, due to the lower property value as a result of forgone development. This, of course, depends on where the property is located.

Obtaining a conservation easement on your land also affects your cost basis in the property. Section 170(h) requires the donor of a conservation easement to allocate a portion of the cost basis in the property to the easement itself. This portion of the cost basis no longer applies to the owner.

An example may make this easier to understand. John originally purchased land for $1 million and now the land is worth $10 million. John obtains a conservation easement on the land and donates it. The easement lowers the property value to $6 million. Under the current tax law rules, the easement itself is valued at $4 million. Since the easement valuation represents 40% of the value of the property, the regulations require that 40% of the cost basis be allocated to the easement. Thus, John’s new basis in the land is $600,000, or 60% of his original $1 million cost basis.

Because of the way an easement affects cost basis, it is important to consider the capital gains tax consequences if you intend to sell the property. If you sell the property during your lifetime, the reduced cost basis could mean you will realize a larger capital gain than you would have without the easement. The potential capital gain will be affected by whether or not the easement drives the sales price down as well.

Individuals who do not plan to sell, however, may not need to worry about the cost basis effect. If you hold the property until your death, the basis of the property will be “stepped up” to its fair market value as of the date of your death, based on current estate tax law. This means that the reduced basis from the easement will have no effect on the tax treatment for your heirs, since their cost basis will be reset regardless of whether the property is subject to an easement or not.

Estate Planning Benefits

The goal of estate planning is to ensure your assets and legacy are protected and transferred according to your wishes well after you are gone. Conservation easements can be a useful component in that plan, as long as you weigh the risks and other potential consequences. If you own land outright and have a passion for environmental protection, a conservation easement may be ideal for your estate plan.

The obvious benefit of conservation easements for estate planning is the protection of the property for all time, regardless of change in ownership. The property can remain in the family indefinitely, and future generations can continue to enjoy its use. Future owners will retain some rights but will be bound by your conservational intentions.

Looking through a functional lens, an easement can help greatly reduce the size of your estate, and thus potential estate tax liability. This benefit is invaluable if the majority of your family wealth is tied up in property and you believe your estate will likely be large enough to be subject to federal gift and estate taxes. In 2024, this means estates larger than $13.61 million per individual. Estate taxes on estates that are largely composed of real property can find the estate tax especially burdensome, since the executor may need to break up or outright sell the land in order to pay the taxes.

Since you and your heirs retain ownership rights, a conservation easement does not remove the land from your estate entirely. However, an easement reduces the land’s value (lowering the value of your overall estate). By granting an easement on your land, you can reduce your estate’s size, possibly preventing your heirs from having to sell the property to raise funds to pay the estate taxes.

Further, the advantage of an estate reduction through an easement will be greater if the estate tax exclusion amount decreases, as it is currently slated to do at the end of 2025. If Congress does not extend the current exemption amount or make it permanent, the exemption will automatically revert back to its pre-Tax Cut and Jobs Act amount of $5 million per estate plus inflation indexing, meaning a limit of roughly $7 million per estate. This expected decrease would mean more Americans need to plan for federal estate taxes again. This would make planning tools, potentially including conservation easements, relevant to more taxpayers.

As with using conservation easements for income tax planning, you should consider carefully when determining if you should include a conservation easement in your estate plan. A conservation easement places permanent restrictions on the development of the land and will reduce its price tag. If these realities align with your goals, they can be upsides, but some landowners may find them frustrating in the long term. The future is not concrete; agreeing to an easement may cause unforeseen issues if circumstances alter. For instance, if the area around your property develops in a way you were not expecting or the needs of your family change, the restrictions on your land may constrict your options. In addition, an easement that allows for public access to the land will impact your family’s privacy on the property going forward.

When you decide whether a conservation easement is the right choice, you must thoroughly consider your personal objectives, the size of your estate, the value of your land, the value of the easement, your selected conservation purposes, and more. It is best to consult your financial planner or estate planning attorney, who can provide a detailed analysis of your estate and an easement’s potential role in it. This will let you make a fully informed decision regarding your valuable property.

Conservation Easement Abuses

Legislators created conservation easements with the intent of encouraging land preservation efforts through tax incentives for participating landowners. However, at the federal level, the proper application of this tax provision has been difficult to enforce and monitor. Beginning in the early 2000s, real estate developers and promoters outside of the traditional land conservation sector became interested in the tax benefits easements allow. Exploitation of the law has spurred the IRS to propose new regulations intended to curb the many abuses. Given the IRS’s position that some taxpayers have been improperly exploiting the benefits conservation easements offer, landowners who want to pursue this strategy in good faith should proceed with caution.

There are two particularly common tactics that attract IRS scrutiny. First, some donors submit inflated, unrealistic appraisals of a conservation easement to increase the associated charitable deduction. Valuing certain types of property — not only land, but also art, businesses, and a variety of other assets — has long been a point of contention between the IRS and taxpayers. Sometimes these are good-faith disputes, but in other cases, disreputable individuals or entities have truly fraudulent intent. Hiring a reputable appraiser and documenting the appraisal thoroughly is therefore critical for taxpayers.

In the second tactic, donors take the charitable deduction for easements that do not fulfill true conservation purposes. These abuses are primarily committed by real estate developers and syndicated conservation easements — tax shelter entities, such as an LLC, which hold a piece of land. Investors seeking a tax deduction buy membership interests in the entity. These partnerships and corporations promote themselves to investors and use the financing from membership interest sales to make nominal improvements on the land. The entity then secures an appraisal (often inflated, in conjunction with the strategy we just discussed) and places a conservation easement on the land under the guise of conservation purposes that are not actually intended. In many cases, investors may believe the conservation purpose is genuine, but fail to perform due diligence or keep a close eye on the syndicate’s operation. The entity’s strategy generates a large and inaccurate charitable deduction, which the entity passes along to the investors, who will take the deduction on their personal tax returns.

Developers or syndicates may, for example, claim conservational intentions but create an agreement that allows developers to stretch any restrictions and overly develop the land. As we mentioned previously, any uses that don’t meet the tax code’s conservation purposes test should disqualify the easement from a potential deduction.

The IRS is aware of such tactics and has introduced new regulations designed to deter the rampant abuses. As part of the SECURE 2.0 Act of 2022, Congress added new sections to Section 170 that provide expanded rules for deductions for charitable contributions. The new rule is aimed at preventing those who attempt to evade taxes through complex ownership structures from taking deductions on overvalued conservation easement contributions. The new restrictions most directly affect partnerships and S corporations, including LLCs that are taxed as partnerships, that make conservation contributions. The change will also affect shareholders in these entities who are allocated a portion of the contributions. Under the new law, deductions are disallowed if the amount of the contribution is more than 250% the sum of each partner or shareholder’s relevant basis in the partnership or S corporation. Additionally, the IRS has instituted expanded reporting requirements for members of an entity who are seeking the deduction. The objective of the new law is to deter inflated appraisals and limit the deduction for real estate developers and others who otherwise might abuse the system. Lawmakers and the IRS have thus taken substantial action to restrict conservation easements to benefiting landowners who genuinely intend their land to be used for conservation purposes.

Since the SECURE 2.0 Act is relatively new, case law is still evolving. New legal precedents have emerged as the U.S. Tax Court and appeals courts have navigated cases centered on the new requirements.

In some cases, the courts have ruled that appraisals were clearly unrealistic, and have disallowed the charitable deduction in its entirety or reduced the deduction to what the court deems a reasonable amount. For instance, in the case of Johnson v. Commissioner, the taxpayer purchased ranch land in Colorado that included a residence and some outbuildings. The property provided a habitat for extensive wildlife including an endangered species, the leopard frog. The taxpayer donated a conservation easement and claimed a $610,000 deduction. The Tax Court ruled that the appraisals that served as the basis of the deduction were materially different from one another and from the relative market for that location, and reduced the easement value by almost 40%.

On the other hand, other courts have upheld deductions that critics have said blur the lines in their commitment to conservation purposes. In Champions Retreat Golf Founders, LLC v. Commissioner, the LLC owned an interest in a golf club in Augusta, Georgia and contributed a land easement over a portion of the land on which the golf course was located. The Tax Court originally disallowed the deduction, but the 11th U.S. Circuit Court of Appeals reversed the decision. The judge did not believe the land the golf course sat on qualified as a “relatively natural habitat,” but the court allowed the deduction because the easement still protected a habitat for several rare, endangered or threatened species of wildlife.

These two cases are a few out of the many that have arisen or are likely to arise around the new rules for conservation easements. Given these changes and the IRS’s interest in stamping out abuse in this area, we recommend that you consult your financial adviser or tax professional if you want to pursue a conservation easement. Professional guidance will help you to avoid potential pitfalls and demonstrate your good-faith compliance under potential IRS scrutiny.

Final Points

Despite abuses in conservation easements and their tax treatment from certain bad actors, easements remain a useful way to protect natural land without fully ceding control of it. The many nuances of tax law and how easements will work in specific scenarios are beyond the scope of this article, but it is likely that regulations and enforcement will continue to evolve. With luck, conservation easements will remain a powerful tax and estate planning tool for landowners who genuinely wish to protect their valuable land for future generations to use and enjoy.