Although young professionals starting their careers may feel they do not have any assets to protect, they are prone to overlook their most precious financial resource — their ability to earn an income.

After graduation, most people are simply satisfied to obtain employment to help manage their newfound responsibilities. Worrying about protecting the few assets they have doesn’t seem as important. However, a good defense is often the best offense.

In the context of financial planning, the aforementioned defense is insurance. Insurance protects against major financial risks that may arise as you travel along the road of life. Most young adults think those risks do not apply to them until they own a home with a white picket fence, get married, and have 2.3 children. On the contrary, insurance is not only for the “established,” but also for the up-and-coming.

People tend to focus on life insurance first. However, during your lifetime, you are more likely to become disabled than you are to die prematurely. Studies by the Social Security Administration show that a 20-year-old has a 3 in 10 chance of becoming disabled for a period of 90 days or more before reaching retirement age. It is clearly important that everyone consider his or her need for disability insurance.

Every second, a disabling injury occurs in the U.S., according to data from the National Safety Council. Most people think accidents cause disabilities, when in reality the majority of disabilities are illness-related. An illness can often lead to increased living expenses, which means that a source of income is still necessary to help cover those costs. If a person is not able to work during his or her illness, the expenses will fall to family and friends. This situation can create an unexpected burden on their finances. Disability insurance helps to mitigate this risk by providing income to a person who is unable to work because of sickness or accidental injury.

Disability insurance can replace up to 80 percent of monthly gross wages, but policies usually pay between 50 percent and 70 percent. Insurers do not provide full income replacement because they want to give the policyholder an incentive to return to work.

Depending on how the insurance premiums were paid, the proceeds from a disability policy may be tax-free. If your employer paid for the disability coverage, or if the premiums were deducted from your wages before taxes, the proceeds are taxable income. If you paid the premiums with after-tax dollars, the insurance proceeds will not be subject to income tax.

Disability insurance coverage is divided into two categories: short-term and long-term disability. Short-term disability insurance generally provides coverage for up to two years. Most policies provide coverage for only a few weeks. Employers typically provide this type of insurance to their employees as a benefit. Long-term disability coverage can provide benefits for a lifetime, or until the insured reaches a certain age, usually 65 or 70.

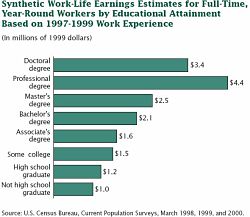

For a young professional, obtaining short-term disability coverage is a step in the right direction, but long-term disability coverage is preferred — especially considering the amount of lost earnings an individual can incur if injured early in his or her career. In a study conducted by the U.S. Census Bureau, researchers estimated that the lifetime earnings of a person with a bachelor’s degree would be $2.1 million. The estimated earnings for master’s, doctoral and professional degrees ranged from $2.5 to $4.4 million (see chart). While the income estimates haven’t been subsequently adjusted from their 1999 levels, they still provide insight on the value of the income that a young professional can expect to earn over a lifetime.

There are standard provisions one should be familiar with when evaluating a disability insurance contract:

Coverage: Policies should provide coverage for accidents and sickness. Though accident-only coverage exists, it is inadequate for most workers. As previously noted, most disabilities are a result of sickness, and an accident-only policy would not provide coverage in those cases. Although premiums for an accident-only policy may be less than the cost of a policy that covers both accidents and sickness, the savings may not be worth the additional risks borne by the insured.

Definition of Disability: This determines whether coverage will apply after any accident, injury, or sickness. Common definitions of disability include:

- Own Occupation — the insured is unable to engage in the occupation he or she had before becoming disabled. This is the most expensive type of policy; but it is essential for some professionals. For example, imagine a brain surgeon who injures his hand and is no longer able to perform surgery. An “own occupation” policy would pay him benefits even though he can work as a medical professor.

- Any Occupation — this policy provides benefits if the insured is unable to engage in any reasonable occupation for which he or she might be suited based on education, experience, training, age, etc.

- Social Security — to qualify for benefits the insured cannot engage in any substantial gainful employment, the disability must have lasted for 5 months and it must be expected to last at least 12 months or result in the death of the worker. This is the most restrictive definition.

Each insurer may have its own take on the aforementioned definitions, so it is important to read the contract carefully and to ask questions. A slight change to the definition of a disability could disqualify our brain surgeon from receiving benefits, even if he purchased an own occupation policy.

Elimination Period: This is the waiting period before the insurer will commence paying benefits. Common elimination periods are 30, 60, 90, and 180 days. The longer the elimination period, the lower the policy premiums. When choosing an elimination period you should ensure you have emergency funds sufficient to cover the elimination period plus another 30 days, because benefits are usually paid at the end of the month following the period.

Benefit Terms: Some disability policies provide benefits for partial disability in addition to total disability. This option is attractive because it will allow you to return to work after a disability, but still provides partial benefits to compensate you if you are not able to return full-time, or if you earn less due to your disability. Whether or not a policy covers partial disability depends on its terms. The definition of partial disability also varies based on the insured’s occupation and the insurer’s definition.

Other benefits include a cost-of-living adjustment (COLA) and an additional purchase benefit (APB). These two benefits are particularly attractive to young professionals. The COLA feature increases the monthly benefit amount based on inflation, which is typically measured by the U.S. Consumer Price Index. This adjustment protects the insured’s purchasing power. The APB allows the insured to purchase additional amounts of insurance at various intervals without having to prove insurability. As you progress through your career, you expect to earn more than when you started. The APB ensures that your insurance coverage is sufficient to support your lifestyle.

The aforementioned benefits may be included in your policy, or you may have to purchase additional riders.

Miscellaneous Provisions: Some disability insurance policies coordinate their benefits with Social Security or workers’ compensation. In both instances, any benefits payable under the policy will be offset by disability payments received under the other programs. It is still a good idea to consider buying a separate disability policy. Social Security’s definition of disability is quite restrictive, and someone just starting a career may not have worked long enough to qualify for benefits. Workers’ compensation only covers injuries that occur in the workplace.

Now that we have covered what to look for in a policy, the next question on your mind is likely the cost. The short answer is that it depends. Insurance companies price policies based on several factors, including your occupation, age, sex and health, along with the length and extent of benefits and the elimination period of the policy.

A general rule of thumb: A policy should cost between 1% and 3% of your gross income. A person earning $60,000 per year can expect to pay yearly premiums between $600 and $1,800. Though this expense may seem prohibitive when you are just starting your career, it may be worth the cost when you consider what you stand to lose.