For small-business owners and self-employed individuals, retirement planning can feel daunting. That doesn’t mean they can afford to neglect it.

Unlike employees, many of whom have access to automatic retirement contributions and HR departments to guide them, the self-employed must take the initiative to research their options, open accounts and fund retirement plans — all while managing the daily demands of operating a business. This added responsibility, combined with sometimes unpredictable income, can lead business owners to delay or avoid retirement planning altogether. Yet failing to act can mean missing tax advantages and losing opportunities for long-term savings growth.

The tax advantages often come from qualified retirement plans. To be qualified, a plan must follow rules laid out by the Employee Retirement Income Security Act, usually shortened to ERISA. While the details of qualified and nonqualified plans are beyond the scope of this article, be aware that tax benefits are usually only available to qualified plans. Depending on the specifics of the plan, contributions can reduce taxable income in the current year, and funds in the plan often grow tax-deferred until retirement.

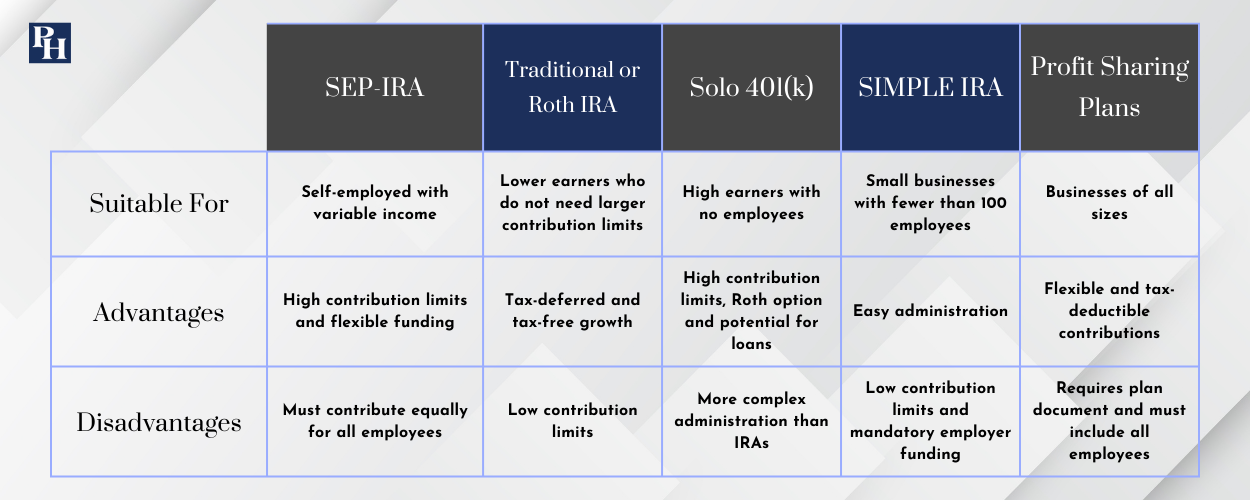

Many plans available to small-business owners also allow owners to build retirement savings while navigating the challenges of unpredictable income. One popular option that offers this flexibility is the simplified employee pension, or SEP IRA.

Understanding Simplified Employee Pensions (SEP IRAs)

A SEP IRA functions similarly to a traditional IRA, but it allows self-employed professionals to make larger contributions and allows business owners to make contributions to employee accounts. The contribution limits are 25% of compensation — up to $350,000 — or $70,000 overall, whichever is less. These dollar amounts apply for 2025, as this threshold is subject to cost-of-living adjustments; for 2024, they were $345,000 and $69,000, respectively. For self-employed workers, compensation is your net earnings less one-half of your self-employment taxes and any contributions you made to your own SEP IRA. Contributions to SEP IRAs are at the discretion of the small-business owner or self-employed individual, meaning the account owner can reduce or skip contributions in years of lower income if they like.

Like a traditional IRA, SEP IRA contributions are made with pre-tax dollars, which means they are tax-deductible for the account owner. Investments within the plan grow tax-deferred, so account owners owe no taxes on investment gains until they make withdrawals. However, distributions from a SEP IRA are taxed as ordinary income, and withdrawals before age 59 ½ may incur a 10% penalty. Additionally, owners must take required minimum distributions, or RMDs, starting at age 73. Since SEP IRA contributions come from the business and not from the individual employee, individuals, including self-employed workers, may contribute to a traditional or Roth IRA in the same year that they receive SEP IRA contributions.

SEP IRAs are an attractive retirement savings option for small-business owners due to their flexibility and high contribution limits. In addition, SEP IRAs generally have low fees. Since a business of any size may establish a SEP IRA, sole proprietors who plan to expand their businesses in the future will be able to add employees to the plan, building in the potential for growth. Note, however, that all eligible employees must be allowed to participate. If you have employees besides yourself, you must also contribute an equal percentage of compensation to all employees’ accounts in any given year. Business owners who wish to differentiate between employees may find other plans more suitable. Employees are also fully vested immediately, so employers cannot use vesting as a retention tool with a SEP IRA plan.

As of 2022, SEP IRA employers are allowed to make Roth contributions: that is, contributing after-tax dollars that account owners will be able to draw income tax free in retirement. However, employers who want to take advantage of this ability will need to ensure their plan custodian allows Roth contributions, as not all of them offer this option. Note, too, that Roth contributions are not tax deductible.

Setting up a SEP IRA is straightforward. Employers will need to pick a financial institution that will serve as the trustee of employee SEP IRAs. They will want to look at details like fees, investment options and customer service availability, much as an individual would if looking to set up a traditional IRA of their own.

Once employers or self-employed individuals have picked a custodian, they must execute a written plan arrangement and provide certain information to employees (if they have any). The form may be a prototype document that the custodian provides or Internal Revenue Service Form 5305-SEP (which employers do not file with the IRS, but rather keep for their own records). Finally, employers should set up an account for each employee to receive contributions. SEP IRA contributions can be made up until the taxpayer’s tax filing deadline, including a six-month extension. This is another advantage over traditional and Roth IRAs, which must be funded by the April filing deadline, regardless of any extensions.

Once established, the administrative burden for a SEP IRA is minimal. There is no ongoing filing requirement, for instance, and custodians generally keep administrative costs low. As with any retirement plan, it is also wise to regularly review your plan to make sure it is operating within the rules and up-to-date with any changes to the law, so you can promptly correct any unintended errors.

Other Options For Freelancers And Business Owners

Traditional Or Roth IRAs

Freelancers with lower contribution needs may find traditional or Roth IRAs a suitable option. Traditional IRAs offer tax-deductible contributions with tax-deferred growth, while Roth IRAs provide no immediate deduction but allow for tax-free withdrawals in retirement. The contribution limit was $7,000 for those under age 50 in 2024 and remained constant for 2025, in both cases with an additional $1,000 catch-up contribution for those age 50 and older. These accounts are ideal for self-employed individuals with relatively low income, who don’t anticipate a need for the higher contribution limits of other retirement plans and thus want to avoid unnecessary administrative costs. As I noted earlier, self-employed workers may also use a traditional or Roth IRA in conjunction with a SEP IRA.

Solo 401(k)s

Self-employed individuals without employees may benefit more from a Solo 401(k), which allows for higher contribution limits than traditional and Roth IRAs. The plan operates similarly to a standard 401(k) operated by a larger organization. Like standard 401(k)s, Solo 401(k)s also allow for Roth contributions, giving flexibility in tax treatment. The 2025 contribution limits are:

- Annual employee deferral: $23,500 ($31,000 for workers 50 or older), up to 100% of compensation, or earned income for a self-employed individual

- Employer discretionary contribution: up to 25% of compensation after Social Security and Medicare taxes, or 20% of earned income for a self-employed individual

- Total maximum contribution: $70,000 ($77,500 for those 50 and older)

The IRS limits the amount of compensation that determines retirement contributions for both employees and employers in the formulas above. For 2025, this limit is $350,000.

Note that, by definition, you will generally be both the employer and the employee, though if your spouse earns income from your business, you may set the plan up for both of you. This means you can make either “employee” or “employer” contributions for the year.

These plans offer the ability to borrow from the account, making them more attractive to those who need savings flexibility than, for example, a SEP IRA. However, a Solo 401(k) requires more administrative effort than many of the other plans in this article, especially if loans are involved.

Contributions to a Solo 401(k) are typically made with pre-tax dollars, providing a deduction that can reduce current taxable income. It is important to note that while traditional Solo 401(k)s reduce federal income tax, they do not reduce self-employment tax. They also allow for tax-deferred growth of investments, and early withdrawals before age 59 ½ may incur a 10% penalty.

Savings Incentive Match Plans For Employees (SIMPLE IRAs)

Small businesses that have fewer than 100 employees and consistent cash flows may be well-suited for a SIMPLE IRA. These plans allow both employers and employees to contribute, and they are relatively easy to set up. However, the contribution limits are significantly lower than those for SEP IRAs and Solo 401(k)s. SIMPLE IRAs are also less flexible than SEP IRAs, as employers must contribute every year, though they may adjust the matching amount to some degree. Businesses cannot offer a SIMPLE IRA along with another employer-sponsored retirement plan.

SIMPLE IRAs allow employee participation in the form of salary deferrals. The amount an employee may defer is determined primarily based on their compensation and their age. For 2025, the employee deferral limit is $16,500, with an additional catch-up contribution of $3,500 for those age 50 and older.

Employees and employers alike gain tax benefits from SIMPLE IRAs. Contributions made by employees are tax-deductible, reducing their taxable income, and grow tax-deferred until withdrawal. Employers can also deduct their contributions on their business tax returns. These contributions may either match employee contributions dollar-for-dollar up to 3% of compensation, or reflect 2% of compensation regardless of employee contributions. Withdrawals from a SIMPLE IRA are taxed as ordinary income, and early withdrawals before age 59 ½ may incur a 10% penalty, increasing to 25% if participants make them within the first two years.

Profit Sharing Plans (PSPs)

Profit-sharing plans allow freelancers and small-business owners to make a discretionary contribution toward retirement savings for employees and themselves. Despite the name, the business need not earn profits for the employer to make a contribution. While profit-sharing plans require a formal plan document and some administrative upkeep, they are relatively straightforward to set up through financial institutions. Only the employer makes PSP contributions, which are typically determined based on the company’s profitability. As a result, these plans are best suited for businesses with fluctuating income, because they give owners the flexibility to decide annually how much they want to contribute, if at all. Note that some plans combine profit sharing and 401(k) features, allowing employee elective deferrals along with employer profit sharing contributions.

For 2025, the total annual contributions to a PSP participant’s account cannot exceed the lesser of $70,000 or 100% of the participant’s compensation for the year. The maximum compensation that can be used to determine contributions is $350,000. Employers may deduct amounts up to 25% of aggregate participant compensation. PSPs are available to businesses of any size and may be used in conjunction with another retirement plan if desired.

click to enlarge

While retirement planning can be challenging for small-business owners and the self-employed, the right retirement plan can significantly enhance their financial security and that of their employees, if they have any. Options like SEP IRAs, Solo 401(k)s and PSPs let business owners tailor their retirement savings strategies to their unique financial situations. And, as always with retirement savings, almost any plan is better than no plan at all.