When managing health care expenses, health insurance is only part of the equation. Whether you have a high-deductible plan or want to build a safety net for unexpected medical costs, flexible spending accounts and health savings accounts can serve as powerful tools to help you keep medical expenses manageable.

What Are These Accounts?

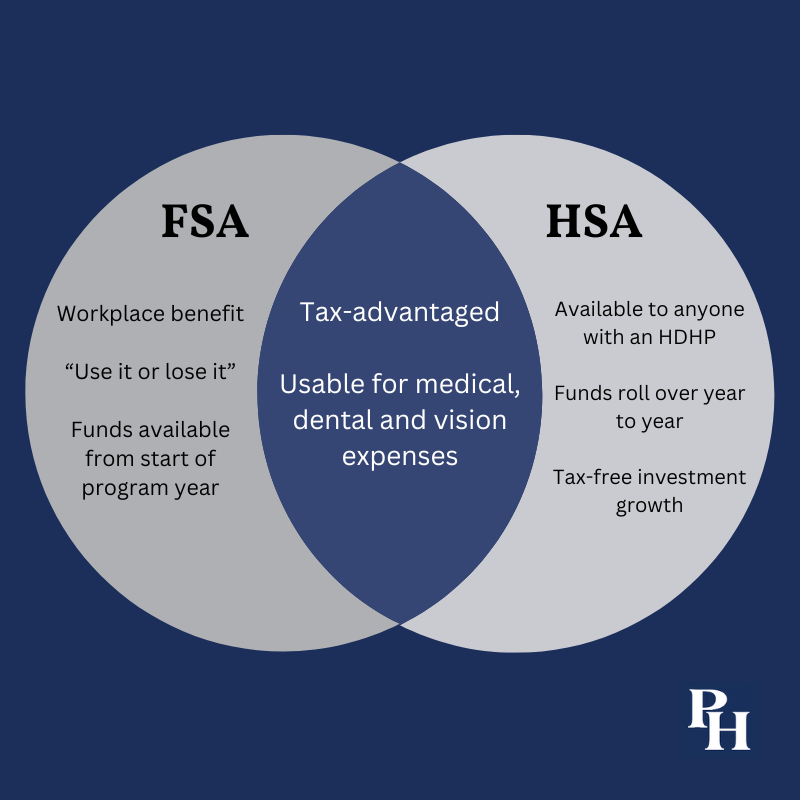

A flexible spending account is an employer-sponsored benefit program that allows employees to set aside pretax dollars for qualified medical expenses. Contributions are deducted directly from the employee’s paycheck. The account holder can use these funds for medical, dental and vision expenses incurred during the plan year. (Some FSAs allow pretax earnings to be used for certain dependent care and adoption expenses, but those plans are outside the scope of this article. We discuss this in slightly more detail in Chapter 13 of our book The High Achiever’s Guide To Wealth.)

A health savings account is a tax-advantaged savings account designed for individuals enrolled in high-deductible health plans. It allows account holders to save and invest pretax dollars for near-term or future medical expenses. Unlike FSA funds, HSA funds roll over from year to year.

Who Can Use FSAs And HSAs?

FSAs are available exclusively through employer benefit plans. Employees at workplaces offering this benefit can elect to contribute a specified amount from their paycheck to their FSA. Think of it as a tax-advantaged savings account specifically for medical expenses.

HSAs can be established directly by individuals enrolled in a high-deductible health plan. For 2025, a high-deductible health plan will be defined as a health insurance plan with a minimum deductible of $1,650 for individual coverage and $3,300 for family coverage, and a maximum out-of-pocket limit of $8,300 for individual coverage and $16,600 for family coverage.

Note that Internal Revenue Service regulations provide that, in most cases, you cannot contribute to an FSA and an HSA in the same year. However, if you opened an HSA in the past before enrolling in an FSA (at a new job, for example), you may keep the HSA open even if you cannot make contributions while participating in the FSA.

How Do These Accounts Work?

Health care costs can be unpredictable, but leveraging the tax advantages of an FSA or HSA can better prepare you for both near-term and future medical needs.

In 2024, you can contribute up to $4,150 for individual coverage and $8,300 for family plans through an HSA. These contribution limits are typically adjusted annually to account for inflation, and for 2025, the limits will increase to $4,300 and $8,550, respectively. Participants can make contributions until April 15 of the following year (so, for example, they can make 2024 contributions until April 15, 2025). If you make these contributions with after-tax dollars, you can deduct them on your federal income tax return. Other people may contribute on your behalf, but the contribution limits are per account, not per contributor.

Similarly, FSA contribution limits allow employees to set aside up to $3,200 ($6,400 per household) in 2024, rising to $3,300 ($6,600 per household) in 2025. As I mentioned previously, participants typically contribute to FSAs through payroll deductions.

Both HSAs and FSAs allow pretax contributions and tax-free withdrawals for qualified medical expenses. However, only HSAs offer the option to invest funds for long-term growth, with earnings also growing tax-free. This advantage means some participants find it useful to treat HSAs as supplementary retirement savings vehicles.

Before you invest your HSA funds, however, it’s important to evaluate how this approach fits into your overall financial strategy. While tax-free growth is appealing, it is important to ensure you maintain enough liquidity for immediate or near-term medical expenses. Can you cover those expenses with other savings in the short term? And as with any account, you should consider investing decisions as part of a comprehensive financial plan, not in isolation. Approaching your HSA investments with your overall financial goals in mind is key for maximizing the account’s benefits.

Understanding which expenses qualify for tax-free withdrawals is also critical to managing your accounts effectively. The IRS defines qualified medical expenses for HSAs and FSAs as those services and products that would generally be deductible as medical expenses on your yearly income tax return. These include, but are not limited to, doctor visits, over-the-counter medicines and prescription drugs, dental expenses and vision expenses for you, your spouse or eligible dependents.

As I mentioned earlier, one of the most significant distinctions between FSAs and HSAs is their flexibility and portability. FSAs have a notable drawback known as the “use it or lose it” rule. Account holders must spend the entire balance by the end of the plan year, or they will forfeit any unused funds to their employer. Some plans offer a grace period of up to 2.5 months to use remaining funds, while others let you carry over up to $640 into the following year. However, employers can only provide one of these options, not both.

Moreover, as an employment benefit, FSAs are tied to your employer. If you leave your job, you cannot transfer the account to a new employer or financial institution. Therefore, make sure you understand the details of your plan before you make any contributions to avoid forfeiting unused funds.

HSAs offer greater flexibility. Unused funds roll over indefinitely, allowing you to accumulate savings (and potentially investment growth) over time. Additionally, HSAs are portable. Because you, and not your employer, oversee the account, an HSA can remain with you regardless of job changes or retirement. This makes HSAs a valuable tool for planning for both current and future health care needs.

How Can You Access Your Funds?

FSA funds become available in full at the beginning of the plan year, regardless of how much you’ve contributed to date. For instance, if you elect to contribute $1,000 annually, that entire amount is accessible on the first day of the plan year. However, every withdrawal must be substantiated as a qualified medical expense. In general, FSAs reimburse expenses you have already incurred and documented. FSAs cannot pay out funds to cover anticipated expenses.

On the other hand, HSA funds are available only as you deposit them into the account. You can either use your HSA to pay qualified medical expenses directly or reimburse yourself for expenses you’ve paid out of pocket. In either case, be sure to maintain detailed records of these expenses in case the IRS requests documentation to support your withdrawals. Withdrawals from an HSA that you use for nonqualified expenses are subject to income tax, plus an additional 20% penalty. Exceptions to this penalty apply if the account holder is 65 or older, becomes disabled or passes away.

An FSA Or An HSA?

In many cases, your circumstances will dictate whether you have access to an FSA or an HSA. Since eligibility for FSAs depends on your employer’s benefits package and HSAs are available only if you’re enrolled in a high-deductible health plan, not everyone will have access to both (or either).

Also remember that even if you qualify for both, you can only contribute to one type of account in a given year. If you are eligible for both an FSA and HSA, evaluating the advantages and limitations of each will help you make an informed choice.

Key factors to consider include:

- Personal health care needs. Consider your expected medical expenses for the year. If you have a chronic condition requiring frequent doctor visits or ongoing medication, an FSA may be a better choice for covering predictable health care costs, especially since the full annual contributions are available when the plan year begins. Be sure to estimate your anticipated expenses carefully to ensure you won’t leave any unused funds behind.

- Alignment with your financial goals. Think about how each account fits into your overall financial strategy. If your primary goal is to build an emergency fund for health care expenses in the future, an HSA could be more advantageous, given that funds can roll over year-to-year and even grow through investments. The HSA’s investment option may also benefit you if you are in generally good health now but want to save for health care expenses in the future.

- Job stability. Your employment situation is an important factor if you are choosing between these accounts. FSAs are tied to your employer, so if you leave your job, you may lose any unused funds when you go. In contrast, HSAs are portable, staying with you even if you change jobs or when you retire. If you anticipate a career transition in the short term or face job uncertainty, an HSA may offer greater flexibility and security.

In conclusion, the best choice will depend on your individual circumstances. FSAs are ideal for short-term health care expenses that can be anticipated within a plan year, while HSAs excel as a long-term savings and investment vehicle for future medical needs.

If you are considering the best plan to choose, or how to use the option available to you to capture the greatest benefit, you may find a meeting with a fee-only financial adviser helpful. The adviser can help you to place these accounts in the context of your overall financial situation.

An FSA or an HSA can offer great, tax-effective ways to handle your health care costs. Given the potential size of health expenses, it is smart to take the time to understand the account or accounts available to you and make sure you are getting the most out of them.